LBBW started the year 2018 with a good first quarter

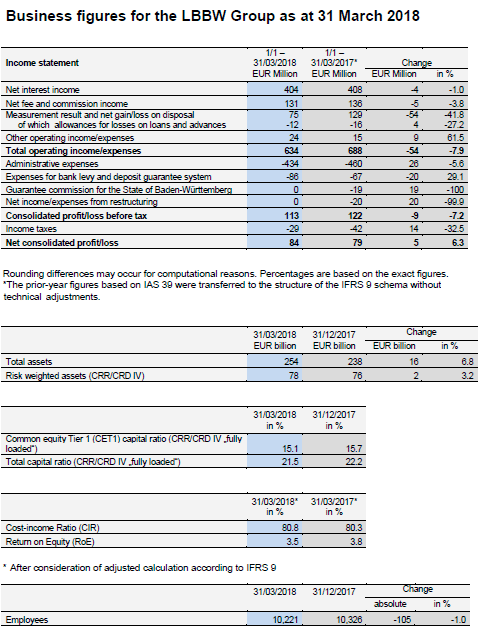

LBBW got off to a good start in 2018 and therefore sustained the positive development of the previous year. Profit before tax in the first quarter amounted to EUR 113 million after EUR 122 million in the same quarter of the previous year. Net profit after tax improved to EUR 84 million (2017: EUR 79 million).

- Profit before tax of EUR 113 million in the first quarter, net profit after tax of EUR 84 million

- Financing and deposit volumes expanded further

- Retail/Savings Banks segment improves result significantly after losses in the previous year

- Administrative expenses decline despite continued high IT investment

- First ever Schuldschein transaction using blockchain technology with a larger number of investors

- LBBW continues to expect profit before tax in the mid-three-digit million euro amount for 2018 as a whole

Business development at the start of the year was defined by particularly intense competition and rising volatility on the capital markets. ”We achieved growth in the lending and deposit businesses in a difficult environment. This allowed us to largely compensate for the charges arising from the low interest rate environment and the high margin pressure. Which demonstrates our ability to perform as a medium-sized universal bank,“ said Rainer Neske, Chairman of the LBBW Board of Managing Directors.

Administrative expenses, which last year were impacted by the change to the core banking system OSPlus, put on a pleasing performance. In addition, LBBW benefited once again from its conservative lending policy in the form of low risk costs. The Bank's capital base also remains very stable: The common equity Tier 1 (CET 1) capital ratio under full implementation of CRD/CRR IV (fully loaded) is 15.1% (31 December 2017: 15.7%), while the total capital ratio is 21.5% (31 December 2017: 22.2 percent). The change is attributable to, among other things, the fact that risk weighted assets increased on the back of lending growth in, for example, the corporate customer business. This is compounded by effects from the equity-reducing first-time application of the new IFRS 9 accounting standard that were adopted as of 1 January 2018.

LBBW continues to make good progress as it works its way through its strategic agenda, the four thrusts of which are business focus, digitalization, sustainability and agility. This is reflected, for example, in the Schuldschein business, an increasingly important pillar of corporate finance. Here, the Bank not only defended its market leadership with 14 transactions in the first quarter, but continued to set benchmarks with further innovations. LBBW and Telefónica Deutschland successfully signed their first blockchain financing in February with double-digit investor numbers involved in the transaction. The project was implemented in a cross-company, interdisciplinary project team. And last but not least, LBBW attracted attention in the area of sustainability as the arranger of the first Green Schuldschein for a real estate company – Volkswagen Immobilien GmbH (VWI) – sized at around EUR 100 million.

The figures at a glance

LBBW is reporting this year for the first time according to the new IFRS 9 accounting standard, resulting in marginal adjustments to the structure of the income statement and selected performance indicators.

At EUR 404 million, net interest income almost reached the figure recorded in the same quarter of the previous year (EUR 408 million). The growth in financing was able to compensate in part for the margin pressure and falling income from own funds investment due to persistently low interest rates.

LBBW achieved net fee and commission income of EUR 131 million, which was in line with the previous year's figure (EUR 136 million). Lower financing commission is offset by higher income from asset management.

At EUR 75 million, measurement result and net gain/loss on disposal were down on the same quarter of the previous year (EUR 129 million). Key components of the item are allowances for losses on loans and advances, net gains/losses on the disposal of securities, investment income/expenses and net gains/losses from financial instruments measured at fair value through profit or loss.

Allowances for losses on loans and advances decreased from EUR – 16 million to EUR – 12 million in the first quarter, reflecting the good portfolio quality and the favorable economy in the core markets. In the period under review LBBW achieved EUR 14 million from the measurement and disposal of securities and equity investments. This result was far below that of the same quarter of the previous year (EUR 58 million), which was defined by high non-recurring income. Net gains from financial instruments measured at fair value through profit or loss came to EUR 72 million (2017: EUR 86 million). The decline is attributable to, among other things, negative valuation effects on counterparty risks (credit valuation adjustments, CVA), which posted a clearly positive development in the prior-year period.

Other operating income improved to EUR 24 million (2017: EUR 15 million), driven mainly by development projects successfully completed by LBBW Immobilien.

Despite continued high investment in the modernization of LBBW´s IT system, administrative expenses fell significantly by EUR 26 million in the first quarter to EUR 434 million. This is not only attributable to high cost discipline but also to unusually high non-recurring costs for the migration to the core banking system OSPlus that impacted on the start of last year.

Expenses for the bank levy and deposit guarantee system increased to EUR 86 million (2017: EUR 67 million). This is due to the higher annual payments to the Single Resolution Fund (SRF) that affect large parts of the financial industry. The expenses expected for the year as a whole have already been absorbed in full in the first-quarter result.

Now that the risks from the special purpose vehicle Sealink no longer exist since the end of 2017, the guarantee commission for the risk shield provided by the State of Baden-Württemberg, which still amounted to EUR 19 million in the prior-year quarter, has been omitted.

Consolidated profit before tax came to EUR 113 million, down from EUR 122 million in the same quarter of the previous year. The income tax expense was reduced by EUR 14 million to EUR 29 million, mainly as a result of lower deferred taxes. Net consolidated profit after tax improved from EUR 79 million to EUR 84 million.

Overview of the operating segments

LBBW rearranged its segments in the course of refining its business focus. The Corporates segment was divided into the Corporate Customers and Real Estate/Project Finance segments. The Capital Markets Business segment largely comprises the business with savings banks, institutional customers and banks, as well as the treasury activities. Business with private customers as well as the meta- and development lending business with savings banks can be found in the Private Customers/Savings Banks segment (previously Retail/Savings Banks).

Lending to medium-sized and large enterprises reported a marked rise in the Corporate Customers segment. LBBW reinforced its strong position even in more complex forms of finance, such as in SME asset securitizations via asset-backed commercial paper, in acquisition finance or in the syndicated lending business. The segment profit nonetheless declined by EUR 19 million before tax to EUR 73 million. This was, besides high margin pressure in the wake of acute price competition, mainly due to the omission of non-recurring income from the disposal of an equity investment in the prior-year quarter and to rising administrative expenses caused by the implementation of regulatory provisions such as MiFID II and growth initiatives, among other things.

The Real Estate/Project Finance segment also expanded its loan portfolio compared with the same quarter of the previous year. This development was supported by a far higher volume of new business in commercial real estate finance with a significant share of certified, sustainable real estate. The order books of the newly established area of project finance, which supports infrastructure projects, renewables and aircraft finance, are filling up noticeably. However, intense competition and low interest rates burdened the segment's net interest income and net fee and commission income. This led to a reduction in the segment profit before tax to EUR 50 million (previous year: EUR 67 million).

The Capital Markets Business segment generated profit before tax of EUR 53 million in the first quarter. In the business with banks and savings banks, LBBW reported consistently high demand for structured notes for private customers of the savings banks and thus remains among the three biggest providers in Germany. Uncertain markets prompted the public sector to exercise restraint in the primary markets business. In this challenging environment, LBBW was able to defend its leading position in, for example, covered bonds or German states (Länder) issues. The fund subsidiary LBBW Asset Management reported a net inflow of funds of almost EUR 3 billion in the first three months and now has around EUR 72 billion in customer funds under management, mainly in special funds for institutional investors. The contribution to earnings from Treasury was substantially lower in the first quarter; in 2017 security sales earnings were generated by using the favorable market environment. This contributed to segment profit before tax of EUR 114 million.

The Private Customers/Savings Banks segment improved its profit before tax in the first quarter significantly to EUR 1 million (2017: EUR – 14 million). This was due mainly to a decline in IT costs following the completed migration to the new core banking system OSPlus, as well as beneficial effects from the reorganization of the private customer business. At the same time, the Bank succeeded in keeping earnings in the retail business almost constant and increasing the volume of customer deposits, despite fierce competition. Demand was particularly strong for investment solutions in the low interest rate environment, such as asset management or fund savings plans as well as for mortgage lending. Further progress was made in the conversion process towards becoming an integrated multi-channel bank. BW-Bank launched Giro worldwide, a free account aimed at young people that can be opened online. The Kwitt function was also integrated in the BW mobile banking app – this allows customers to transfer smaller sums of money from one smartphone to another, easily, securely and in real time. Not least, the close cooperation with the savings banks once again led to record volumes in the area of development lending. After only three months, the volume of new business stood at EUR 2 billion, thanks to the strong demand for innovation and digitalization financing.

Outlook

For the year as a whole, LBBW continues to forecast consolidated profit before tax in the mid-three-digit million euro amount.

Downloads

-

32.3 KB | 29.06.2018

-

68.3 KB | 29.05.2018

{kind=link}