August 29, 2025

US equity market: all bets are on one card!

High valuation and high concentration call for caution.

To the point!

LBBW Research is confident that artificial intelligence will have a significant productivity-enhancing effect in many areas. At the same time, however, we remain cautious in view of the high valuations and advise a rather defensive positioning.

The stock markets, especially in the USA, seem to be unperturbed by anything. In the last two years alone, the S&P 500 index has risen by over 45%, and by over 80% in the last five years. In the last decade by over 220%! Great for those who were fully invested. Congratulations!

There have always been setbacks that put investors' nerves to the test. Most recently after Donald Trump's surreal "Liberation Day" at the beginning of April. But then the "TACO trade" gained the upper hand again: Trump Always Chickens Out – Trump always chickens out. It won't be that bad...

The final positive impetus came from Trump's favourite enemy, Federal Reserve Chairman Jay Powell, when he waved a fence post in Jackson Hole last week and opened the door wide for an interest rate cut in mid-September.

Irrational exuberance 2.0?

There is a growing danger that the sheer boundless optimism of investors will turn into naivety. The premise that presidents who bark don't bite seems increasingly naive to me. With his behaviour, most recently with the grandiloquently announced dismissal of Fed Governor Lisa Cook (for which he has no legal basis) or the unilateral ignoring of supposed tariff agreements with the EU, the President is demonstrating that he is not in the mood for jokes. The TACO trade is therefore risky. It is said that barking dogs have bitten after all. Trump seems to me to be such a barking dog.

The risks of Trumponomics are still being smiled away

The increasingly lofty valuations of US equities therefore also mark growing drop heights should something unfortunate happen. A simple measure of the high valuation is the so-called Warren Buffet indicator. It measures the market value of stock corporations as a multiple of the US national product. At the peak of the dot.com bubble, this value was a historically high 1.5. Today, the market value of stock corporations exceeds 2.1 times the annual US value added.

The US stock market is extremely concentrated

However, the comparison with the internet bubble is not entirely fair. In contrast to back then, today's tech giants have high (and growing) profits. This was not the case for most of the Internet hopefuls at the turn of the millennium. At the same time, however, the market is much more concentrated today than it was back then. The ten largest stocks in the S&P 500 account for 40% of market capitalisation (see Fig. 1). The remaining 490 just account for the remaining 60 %.

Fig. 1: Market capitalisation of the top 10 companies as a share of the S&P 50

in %

Such a concentration is without historical parallel. In contrast to the meteoric rise of AI shares, the valuation of the average company in the S&P 500 has fallen back to the level of 2003 ! There is stagnation across the market. The rally is being driven by fewer and fewer stocks.

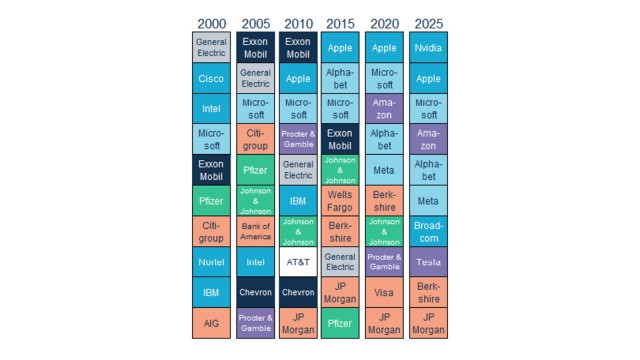

There is also an extreme concentration of sectors. Eight of the ten most valuable companies are technology groups whose high valuations are consistently driven by immense hopes for the expected blessings of artificial intelligence (see Fig. 2). But also by the expectation that the immense investments, for example in data centres, will remain high-margin. However, if the market for AI services becomes more competitive than is currently the case, then the tech giants will all be in the same leaky boat. The brief DeepSeek shock at the beginning of the year now seems to have been forgotten. Investors seem to think it is almost impossible that the current AI kings could be toppled from their thrones. The fact that Sam Altman of all people, founder and CEO of OpenAI, the company behind ChatGPT, recently spoke of AI stocks being caught up in a speculative bubble is also rubbing off on investors. As long as the music plays, the dancing will continue.

Composition of the top 10 stocks in the S&P 500 by market capitalisation

Fig. 2

LBBW Research is confident that artificial intelligence will have a significant productivity-enhancing effect in many areas. At the same time, however, we remain cautious in view of the high valuations and recommend a rather defensive positioning. We see the S&P 500 Index ending the year at 6200 points, from a current index value of 6466.

Dr. Moritz Kraemer, Chief Economist / Head of Research at LBBW

Download To the point!

-

278.0 KB | August 29, 2025

This publication is addressed exclusively at recipients in the EU, Switzerland, Liechtenstein and the United Kingdom.

This report is not being distributed by LBBW to any person in the United States and LBBW does not intend to solicit any person in the United States.

LBBW is under the supervision of the European Central Bank (ECB), Sonnemannstraße 22, 60314 Frankfurt/Main (Germany) and the German Federal Financial Supervisory Authority (BaFin), Graurhein-dorfer Str. 108, 53117 Bonn (Germany) / Marie-Curie-Str. 24-28, 60439 Frankfurt/Main (Germany).

This publication is based on generally available sources which we are not able to verify but which we believe to be reliable. Nevertheless, we assume no liability for the accuracy and completeness of this publication. It conveys our non-binding opinion of the market and the products at the time of the editorial deadline, irrespective of any own holdings in these products. This publication does not replace individual advice. It serves only for informational purposes and should not be seen as an offer or request for a purchase or sale. For additional, more timely in-formation on concrete investment options and for indi-vidual investment advice, please contact your investment advisor.

We retain the right to change the opinions expressed herein at any time and without prior notice. More-over, we retain the right not to update this information or to stop such updates entirely without prior notice.

Past performance, simulations and forecasts shown or described in this publication do not constitute a reliable indicator of future performance.

The acceptance of provided research services by a securities services company can qualify as a benefit in supervisory law terms. In these cases LBBW assumes that the benefit is intended to improve the quality of the relevant service for the customer of the benefit recipient.

Additional Disclaimer for recipients in the United Kingdom:

Authorised and regulated by the European Central Bank (ECB), Sonnemannstraße 22, 60314 Frank-furt/Main (Germany) and the German Federal Financial Supervisory Authority (BaFin), Graurheindorfer Str. 108, 53117 Bonn (Germany) / Marie-Curie-Str. 24-28, 60439 Frankfurt/Main (Germany). Authorised by the Prudential Regulation Authority. Subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request.

This publication is distributed by LBBW to professional clients and eligible counterparties only and not retail clients. For these purposes, a retail client means a person who is one (or more) of (i) a client as defined in point (7) of Article 2(1) of the UK version of Regulation (EU) 600/2014 which is part of UK law (UK MiFIR) by virtue of the European Union (Withdrawal) Act 2018 (EUWA) who is not a professional client (as defined in point (8) of Article 2(1) of UK MiFIR); or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000 (as amended, the FSMA) and any rules or regulations made under the FSMA (which were relied on immediately before the 31 December 2020 (IP completion day)) to implement Directive (EU) 2016/97 on insurance distribution, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of UK MiFIR; or (iii) not a qualified investor as defined in the UK version of Regulation (EU) 2017/1129 on the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, which is part of UK law by virtue of the EUWA (the UK Prospectus Regulation).

This publication has been prepared by LBBW for information purposes only. It reflects LBBW’s views and it does not offer an objective or independent outlook on the matters discussed. The publication and the views expressed herein do not constitute a personal recommendation or investment advice and should not be relied on to make an investment decision. The appropriateness of a particular investment or strategy will depend on an investor’s individual. You should make your own independent evaluation of the relevance and adequacy of the information contained in this publication and make such other investigations as you deem necessary, including obtaining independent financial advice, before partici-pating in any transaction in respect of the financial instruments referred to this publication herein.

Under no circumstance is the information contained within such publication to be used or considered as an offer to sell or a solicitation of an offer to buy any particular investment or security. Neither LBBW nor any of its subsidiary undertakings or affiliates, directors, officers, employees, advisers or agents accepts any responsibility or liability whatsoever for/or makes any representation or warranty, express or implied, as to the truth, fullness, accuracy or completeness of the information in this publication (or whether any information has been omitted from the publication) or any other information relating to the, whether written, oral or in a visual or electronic form, and howsoever transmitted or made available or for any loss howsoever arising from any use of this publication or its contents or otherwise arising in connection therewith.

The information, statements and opinions contained in this publication do not constitute or form part of a public offer. LBBW assumes no responsibility for any fact, recommendation, opinion or advice con-tained in any such publication and expressly disclaims any responsibility for any decisions or for the suitability of any security or transaction based on it. Any decisions that a professional client or eligible counterparty may make to buy, sell or hold a security based on such publication will be entirely their own and not in any way deemed to be endorsed or influenced by or attributed to LBBW.

LBBW does not provide investment, tax or legal advice. Prior to entering into any proposed transaction on the basis of the information contained in this publication, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences, of the transac-tion.