July 17, 2026

Will the music stop?

The risk of a stock-market correction has been growing.

To the point!

After three bumper years in which Germany’s DAX stock index rose by a little over 20% each time, this year has also been kind to shareholders so far. The DAX itself has barely budged, but the U.S. S&P 500 is up by more than 10%, and the tech-heavy Nasdaq has climbed further still.

The Strait of Hormuz blocked? Never mind – that will pass. Higher long-term interest rates? So what – booming earnings will more than offset them. Nothing seemed able to unsettle investors’ bullish mood. In their eyes, the glass was not merely half full; it was nowhere near big enough.

Volatility is back

But in June the wind began to shift. AI-related market darlings were buffeted by rising volatility (see fig. 1). And even when earnings growth remained robust, investors often sent shares diving.

Now the backdrop is becoming more difficult still. Hopes for an end to the war with Iran have once again faded. In bond markets, interest-rate expectations have risen accordingly. That weighs on growth stocks in the tech sector, because investors will now discount their future earnings at a higher rate.

Fig. 1: Volatility among the 50 largest technology stocks globally

⬤ {series.name}: {point.y}

We are not in a repeat performance of the dotcom bubble

To be clear: this is not the same situation as at the turn of the millennium, when the internet bubble burst. Back then, companies with no profits – and often no prospect of making any – fired investors’ imaginations. Analysts like us watched indicators such as the “cash-burn rate”, meaning how quickly the would-be internet stars were burning through capital. Today’s AI giants, by contrast, are highly profitable and have real business models.

Yet this much is also true: market concentration in a handful of stocks is far higher today than it was in 2000. The ten largest companies – almost all of them in technology – now account for more than 40% of the S&P 500’s total market capitalization. In 2000 the figure was only around 25%. Back then, the biggest stocks were also spread more evenly across sectors. Today, all the chips are on AI. If those lofty expectations are disappointed, the risk of a correction is substantial.

Is a tsunami of IPOs on the way?

After years in which buybacks steadily reduced the supply of shares, a flood of new equity is now hitting the market (see fig. 2). SpaceX and South Korean chipmaker SK Hynix recently launched the largest share offerings ever in the U.S. market; SK Hynix did so through a secondary listing. OpenAI and Anthropic are likely to follow soon. Why are these companies’ owners of-fering shares to the public? Surely not because they think the shares are undervalued.

Fig. 2: Net equity issuance

2000-2027e. in $bn

NB: 2027 are estimates with the lat-ter reflecting estimated free float change from big IPOs.

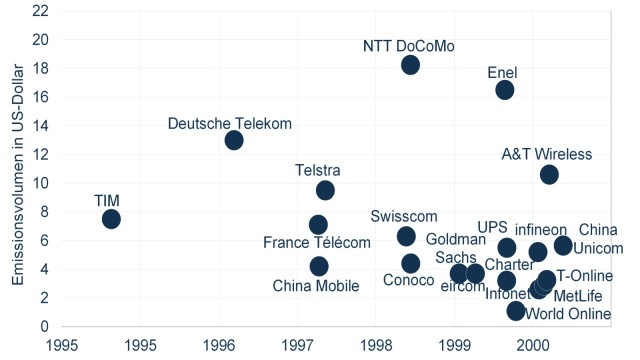

The hyperscalers are indeed profitable. Alas, the same cannot be said of companies such as SpaceX or OpenAI. Some are running up substantial losses, and new shareholders are buying mainly the promise of future profitability. In that respect, today’s market does bear some resemblance to the period before the dotcom bubble burst. Back then, too, dizzying valuations encouraged an unusually large number of companies to go public (see fig. 3). Once the bubble burst, shareholders were left nursing the losses. Germany saw a similar pattern in the Neuer Markt, the country’s late-1990s growth-stock segment. Investors were not buying profits; they were buying stories. And quite a few of those stories later turned out to be fairy tales.

Fig. 3: POs with proceeds above $1bn, early 1995 to end-2000

More stock, same buyers?

Not only have recent weeks brought the two largest IPOs in U.S. stock-market history. More giant offerings may follow. In both mega-IPOs, the owners sold only a relatively small stake. In SpaceX’s case, for example, only about 5% of the stock was sold. That is a fraction of the typical IPO float. Once the standard six-month lock-up period expires, existing owners such as Elon Musk can sell their own shares. That would leave the market with still more stock to absorb. And we all know what happens when rising supply meets steady demand. Exactly: prices fall. This is not my forecast, and LBBW Research’s base case does not call for a market correction. But the risks associated with high valuations and market concentration have undoubtedly grown. That Bank of America’s Global Fund Manager Survey shows U.S. equity positions at their largest overweight since late 2024 makes me a little nervous. So does the fact that a long position in global semiconductor stocks remains the most crowded trade. If everyone is bullish already, where will future stock buyers come from?

Be careful and stand clear of the platform edge!

Dr. Moritz Kraemer, Chief Economist / Head of Research at LBBW

Download To the point!

-

1.1 MB | July 17, 2026

This publication is addressed exclusively at recipients in the EU, Switzerland, Liechtenstein and the United Kingdom.

This report is not being distributed by LBBW to any person in the United States and LBBW does not intend to solicit any person in the United States.

LBBW is under the supervision of the European Central Bank (ECB), Sonnemannstraße 22, 60314 Frankfurt/Main (Germany) and the German Federal Financial Supervisory Authority (BaFin), Graurhein-dorfer Str. 108, 53117 Bonn (Germany) / Marie-Curie-Str. 24-28, 60439 Frankfurt/Main (Germany).

This publication is based on generally available sources which we are not able to verify but which we believe to be reliable. Nevertheless, we assume no liability for the accuracy and completeness of this publication. It conveys our non-binding opinion of the market and the products at the time of the editorial deadline, irrespective of any own holdings in these products. This publication does not replace individual advice. It serves only for informational purposes and should not be seen as an offer or request for a purchase or sale. For additional, more timely in-formation on concrete investment options and for indi-vidual investment advice, please contact your investment advisor.

We retain the right to change the opinions expressed herein at any time and without prior notice. More-over, we retain the right not to update this information or to stop such updates entirely without prior notice.

Past performance, simulations and forecasts shown or described in this publication do not constitute a reliable indicator of future performance.

The acceptance of provided research services by a securities services company can qualify as a benefit in supervisory law terms. In these cases LBBW assumes that the benefit is intended to improve the quality of the relevant service for the customer of the benefit recipient.

Additional Disclaimer for recipients in the United Kingdom:

Authorised and regulated by the European Central Bank (ECB), Sonnemannstraße 22, 60314 Frank-furt/Main (Germany) and the German Federal Financial Supervisory Authority (BaFin), Graurheindorfer Str. 108, 53117 Bonn (Germany) / Marie-Curie-Str. 24-28, 60439 Frankfurt/Main (Germany). Authorised by the Prudential Regulation Authority. Subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request.

This publication is distributed by LBBW to professional clients and eligible counterparties only and not retail clients. For these purposes, a retail client means a person who is one (or more) of (i) a client as defined in point (7) of Article 2(1) of the UK version of Regulation (EU) 600/2014 which is part of UK law (UK MiFIR) by virtue of the European Union (Withdrawal) Act 2018 (EUWA) who is not a professional client (as defined in point (8) of Article 2(1) of UK MiFIR); or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000 (as amended, the FSMA) and any rules or regulations made under the FSMA (which were relied on immediately before the 31 December 2020 (IP completion day)) to implement Directive (EU) 2016/97 on insurance distribution, where that customer would not qualify as a professional client, as defined in point (8) of Article 2(1) of UK MiFIR; or (iii) not a qualified investor as defined in the UK version of Regulation (EU) 2017/1129 on the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, which is part of UK law by virtue of the EUWA (the UK Prospectus Regulation).

This publication has been prepared by LBBW for information purposes only. It reflects LBBW’s views and it does not offer an objective or independent outlook on the matters discussed. The publication and the views expressed herein do not constitute a personal recommendation or investment advice and should not be relied on to make an investment decision. The appropriateness of a particular investment or strategy will depend on an investor’s individual. You should make your own independent evaluation of the relevance and adequacy of the information contained in this publication and make such other investigations as you deem necessary, including obtaining independent financial advice, before partici-pating in any transaction in respect of the financial instruments referred to this publication herein.

Under no circumstance is the information contained within such publication to be used or considered as an offer to sell or a solicitation of an offer to buy any particular investment or security. Neither LBBW nor any of its subsidiary undertakings or affiliates, directors, officers, employees, advisers or agents accepts any responsibility or liability whatsoever for/or makes any representation or warranty, express or implied, as to the truth, fullness, accuracy or completeness of the information in this publication (or whether any information has been omitted from the publication) or any other information relating to the, whether written, oral or in a visual or electronic form, and howsoever transmitted or made available or for any loss howsoever arising from any use of this publication or its contents or otherwise arising in connection therewith.

The information, statements and opinions contained in this publication do not constitute or form part of a public offer. LBBW assumes no responsibility for any fact, recommendation, opinion or advice con-tained in any such publication and expressly disclaims any responsibility for any decisions or for the suitability of any security or transaction based on it. Any decisions that a professional client or eligible counterparty may make to buy, sell or hold a security based on such publication will be entirely their own and not in any way deemed to be endorsed or influenced by or attributed to LBBW.

LBBW does not provide investment, tax or legal advice. Prior to entering into any proposed transaction on the basis of the information contained in this publication, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences, of the transac-tion.